Sigmaintell Global Display Strategic Outlook Seminar detail

Sigmaintell Global Display Strategic Outlook Seminar detail

Sigmaintell Global Display Strategic Outlook Seminar detail

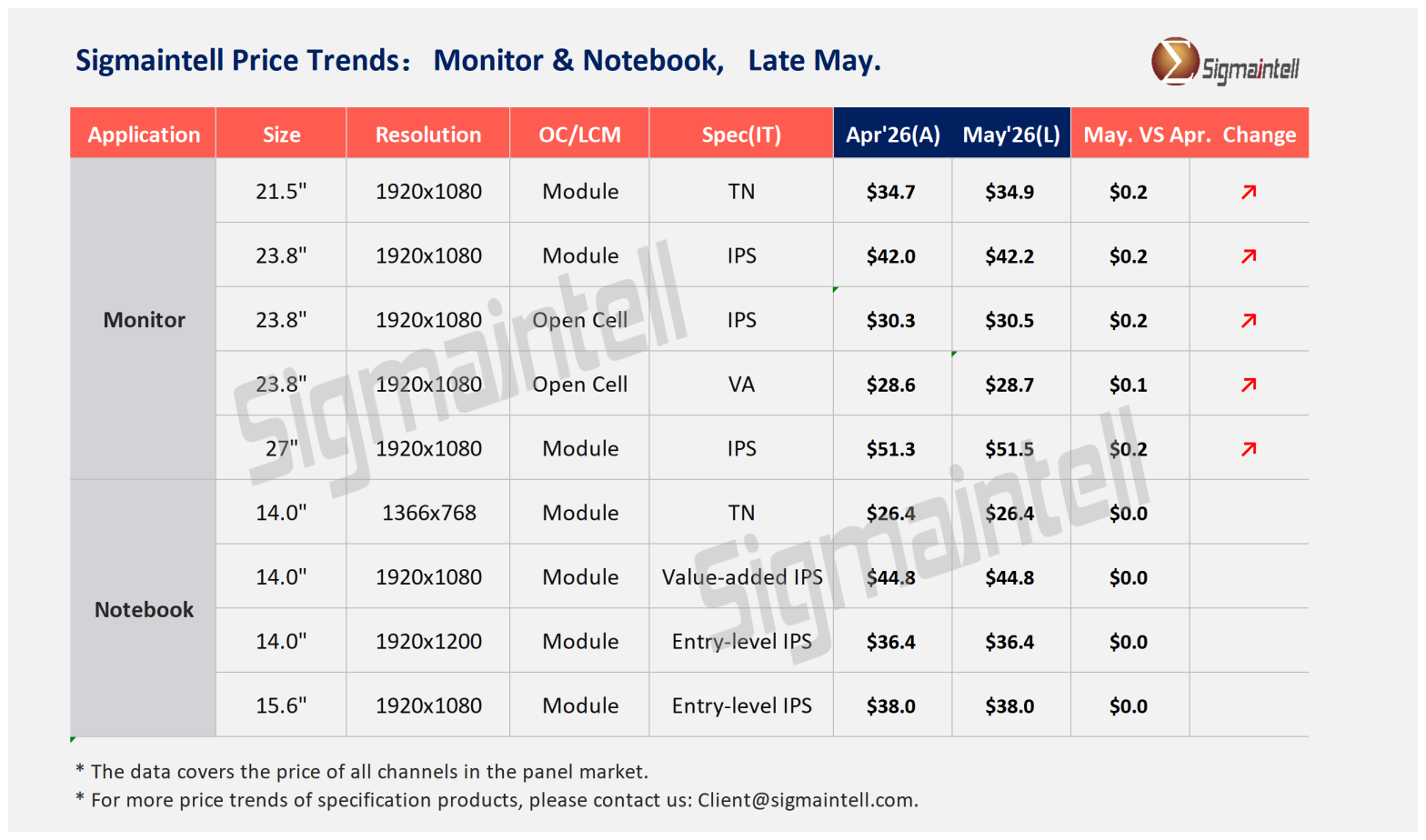

In May, global monitor panel prices continued their upward trend, with the MoM price increases of mainstream specifications narrowing moderately, as the industry entered a critical period of supply and demand gaming. Driven by the combined effects of a structurally tight supply and demand landscape, continuous rises in upstream material prices, and further increased concentration in panel supply, the monitor panel market is set to maintain its price upward trajectory.

Sigmaintell Global Display Strategic Outlook Seminar detail

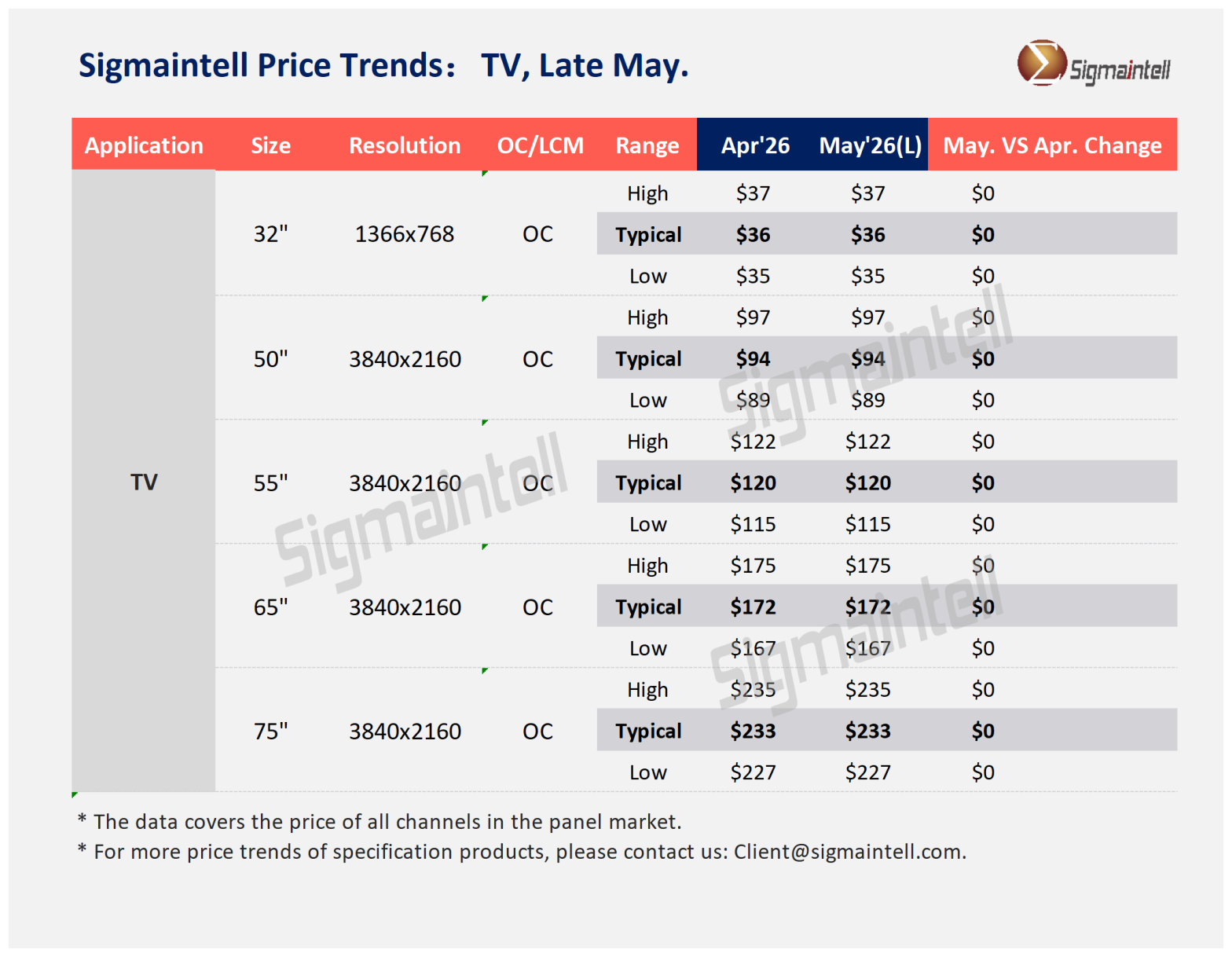

As of May, the pace of demand-side adjustments has slowed, with the global TV panel market maintaining a static equilibrium. From the perspective of panel demand, following the conclusion of both sports event-related stocking and the first-half promotion inventory buildup, brand vendors have largely completed deep adjustments to their second-quarter procurement strategies, resulting in a sequential softening of overall stocking momentum.

The global technological competition landscape continues to evolve, with trade controls, supply chain security and technical barriers profoundly impacting the high-end display industry chain. For a long time, core OLED materials have been highly dependent on imports; overseas enterprises have dominated relying on technological, patent and ecological advantages, becoming a key constraint on the independent control of the display industry.

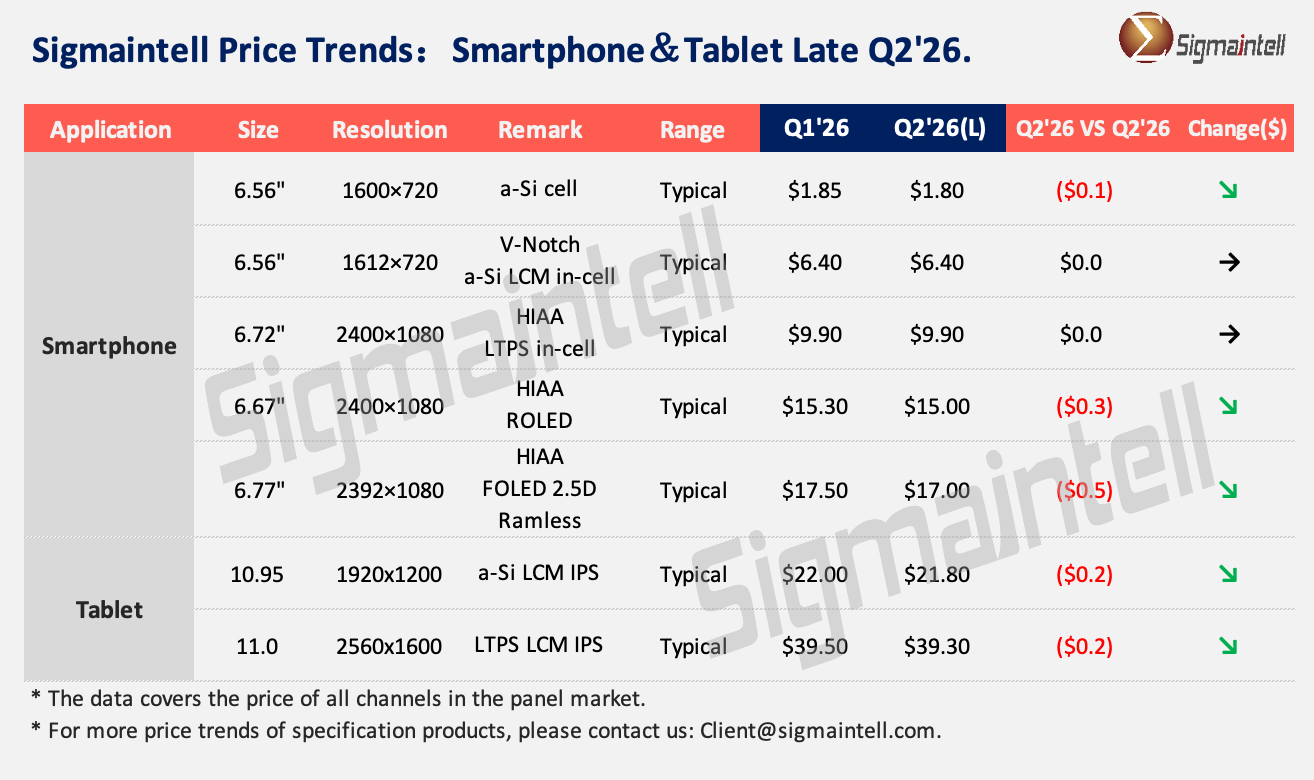

In Q2 2026, the global smartphone display panel market continued to grapple with sluggish demand, maintaining an oversupplied and loose overall market landscape. The industry faced tough headwinds amid high costs and weak demand. While overall panel prices remained stable, divergent trends emerged significantly across different technology segments.

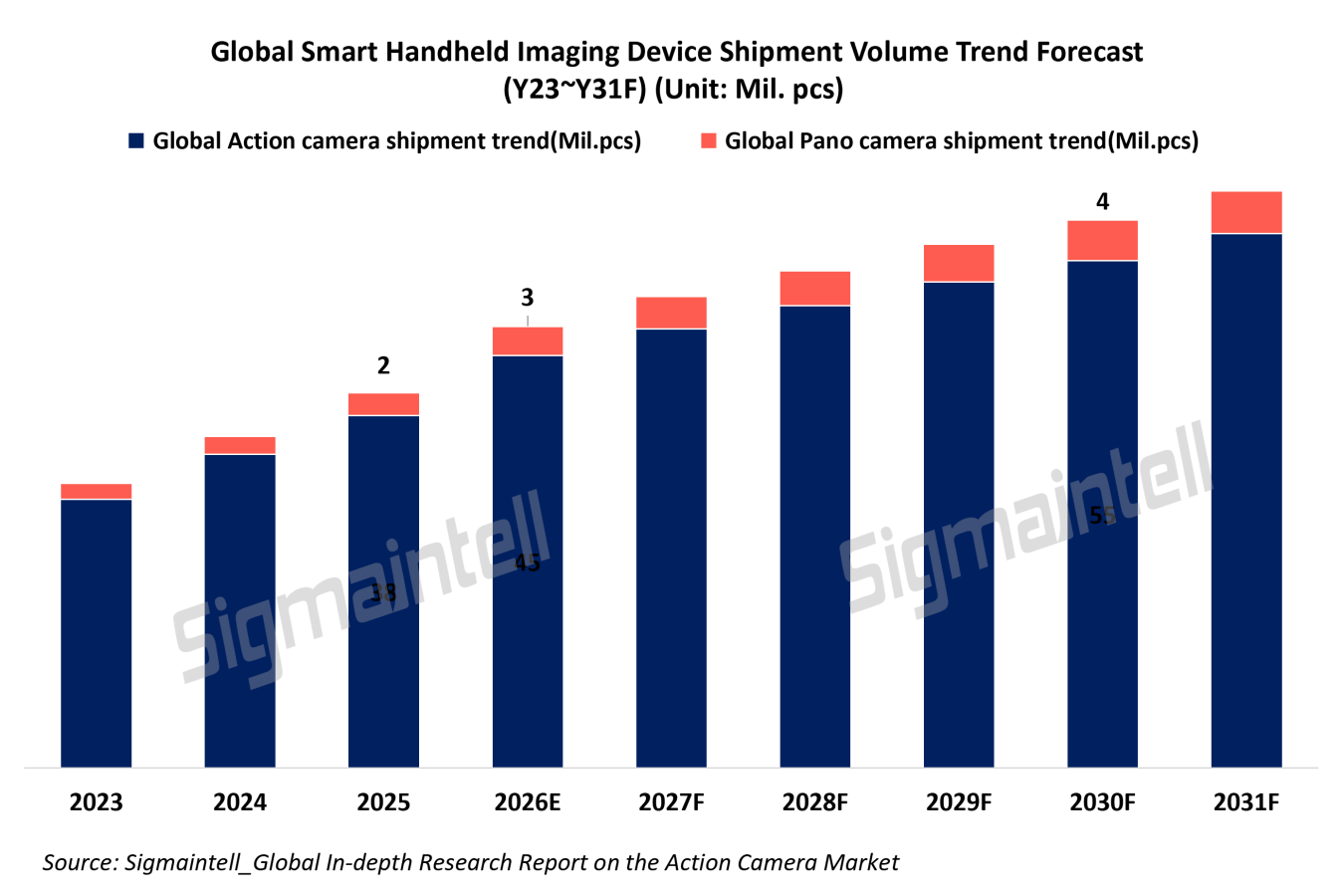

From bulky early cameras to today’s lightweight Smart Handheld Imaging Devices, technological advances are redefining how we capture the world. Data shows the global market size of Smart Handheld Imaging Devices will grow from 29.12 million units in 2023 to 57.90 million units in 2031, representing a CAGR of 9.1% and demonstrating robust market vitality. The sector is embracing unprecedented development opportunities.

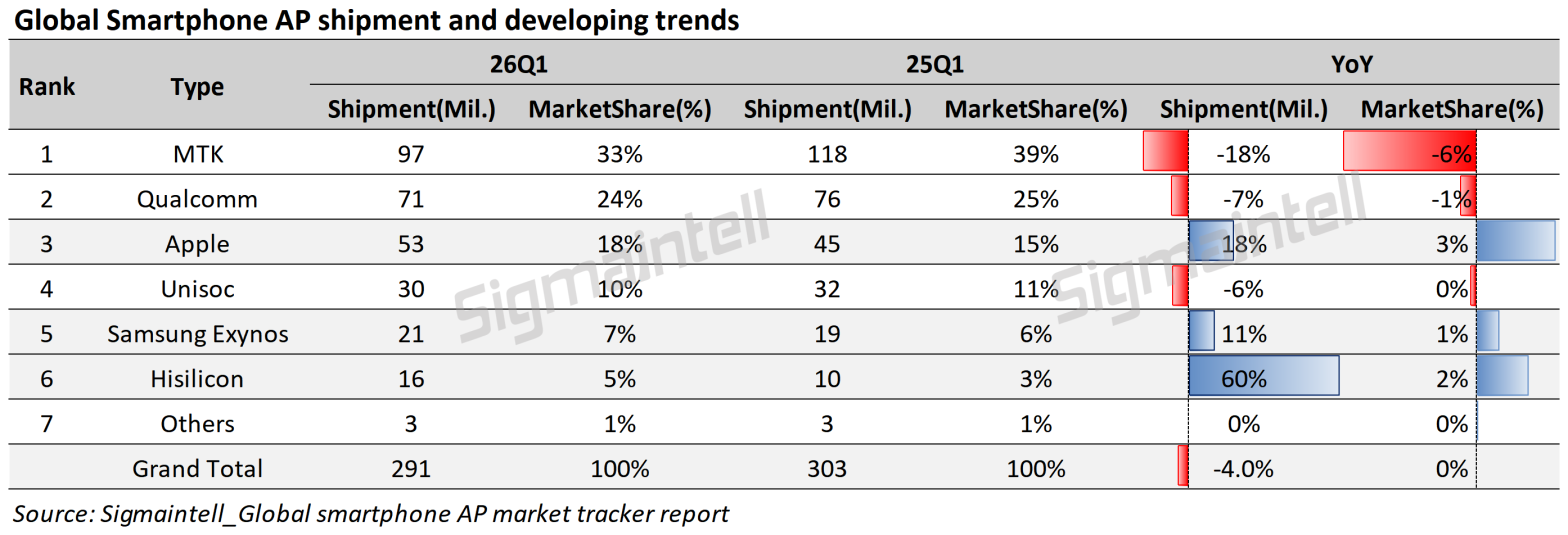

Driven by the sustained pass-through effect of memory chip price increases to overall handset manufacturing costs, global demand for smartphone Socs contracted in the first quarter of 2026. Against this backdrop, the market witnessed a notable structural divergence: leading players with in-house chip design capabilities achieved counter-trend growth by leveraging vertical integration and ecosystem advantages, while traditional third-party chip design firms faced severe challenges.

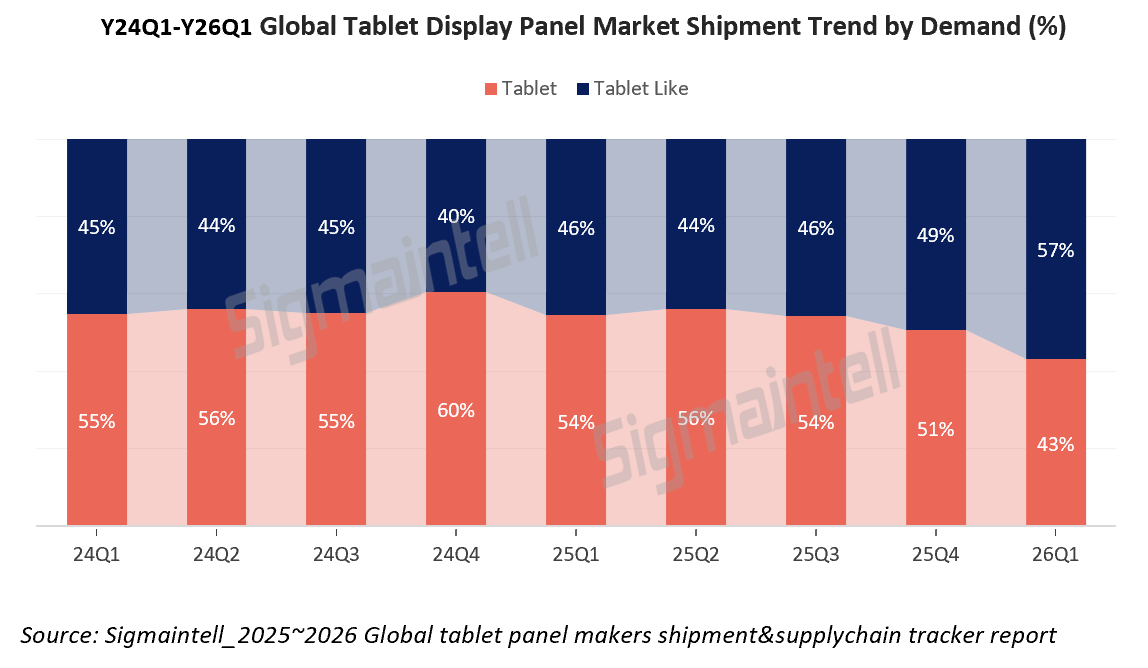

According to Sigmaintell data, global tablet panel shipments reached approximately 70.6 million units in Q1 2026, registering a slight YoY increase. However, this “stable” headline conceals significant structural distortion: on the demand side, the branded segment declined approximately 21.1% YoY, while South China demand surged approximately 25.0% YoY, adding nearly 8 million units in a single quarter. These two opposing forces offset one another, masking the true displacement of demand. This divergence is not a conventional contest between strong and weak brands; rather, it stems from the differing sensitivity of the two markets to memory cost pass-through, and the resulting reconfiguration of supply-demand structure. The “flat” Q1 2026 print should be read as the starting point of a deep divergence phase, not as a continuation of equilibrium.