Tag :Application, Semiconductor

Time :2026-5-14

Foreword:

Driven by the sustained pass-through effect of memory chip price increases to overall handset manufacturing costs, global demand for smartphone Socs contracted in the first quarter of 2026. Against this backdrop, the market witnessed a notable structural divergence: leading players with in-house chip design capabilities achieved counter-trend growth by leveraging vertical integration and ecosystem advantages, while traditional third-party chip design firms faced severe challenges.

With memory costs remaining elevated and demand broadly under pressure, global Soc shipments fell approximately 4% YoY in Q1.

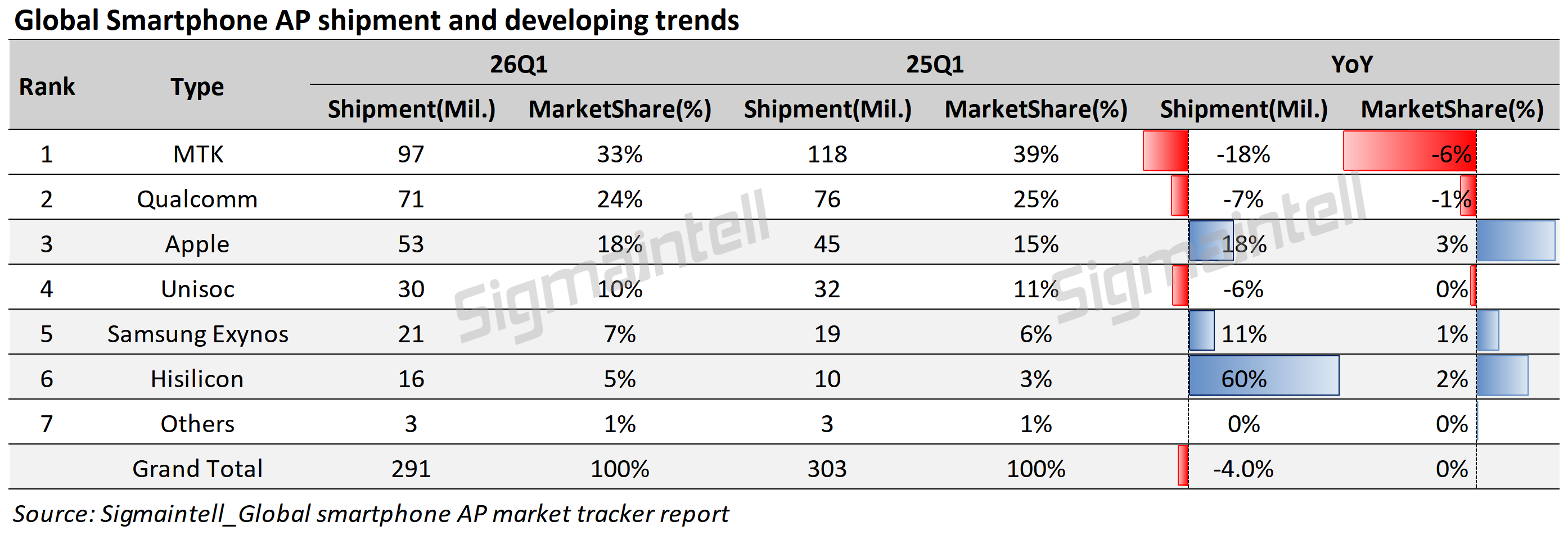

Since the second half of 2025, the sustained surge in memory chip prices, driven by AI server demand, has continued to propagate through the supply chain, directly pushing up smartphone production costs. According to data from Sigmaintell, total global smartphone Soc shipments reached approximately 290 million units in the first quarter of 2026, representing a YoY decline of about 4.0%. The mid-to-low-end segment, which primarily targets price-sensitive consumers, bore the brunt of the impact. Rising end-product prices stemming from higher component costs dampened consumer demand, prompting brands to scale back inventory and chip procurement. The decline in sales was particularly pronounced in the smartphone segment priced below 1,000 yuan.

Vendor performance diverged: MediaTek and Qualcomm encountered growth challenges, while the share of shipments from in-house designed chips posted counter-trend growth.

From a vendor-specific perspective, traditional chip giants faced growth headwinds. The shipment volumes of leading players MediaTek and Qualcomm both declined YoY. According to data from Sigmaintell, MediaTek and Qualcomm shipped 97 million and 71 million smartphone Socs in the first quarter of this year, representing YoY declines of approximately 18% and 7%, respectively.

In stark contrast, vendors with in-house chip capabilities achieved counter-trend shipment growth, fully demonstrating their competitive advantages. This contrast not only highlights the strengths of proprietary chips but also confirms that, in times of market volatility, in-house chip capabilities have become a critical pillar for manufacturers to mitigate risks and drive growth, laying the foundation for sustained shipment increases.

The counter-trend growth in shipments of in-house chips reflects the full manifestation of their comprehensive core competitive advantages. Shipment data from the three major in-house chip vendors—Apple, Samsung, and Huawei—directly validates this core logic, with each company achieving breakthrough growth in different dimensions by leveraging their distinct strengths.

Apple, as the benchmark of in-house chip design, achieved steady growth amid an industry-wide downturn. According to data from Sigmaintell, its smartphone chip shipments reached approximately 53 million units in the first quarter of this year, up about 17.8% YoY. The core advantages underpinning this growth lie in the deep alignment between its in-house chips and premium devices, the synergistic empowerment of its closed ecosystem, and autonomous cost control. By precisely matching the performance and experience demands of high-end users, integrating seamlessly with iOS to deliver differentiated user experiences, and independently managing R&D, production, and supply cadence, Apple effectively mitigated cost pressures stemming from memory price hikes, thereby driving steady shipment growth.

Samsung Exynos leveraged the dual strengths of its in-house chips and fully integrated vertical supply chain to defend its shipment base amid the industry downturn. In the first quarter of 2026, Samsung Exynos smartphone chip shipments reached 21 million units, representing a YoY increase of approximately 11%. The strong performance of the Galaxy S26 series also played a positive role in boosting Exynos shipments. As a player with end-to-end capabilities spanning chip design, manufacturing, and packaging/testing, Samsung is able to perfectly tailor its in-house chips to its own devices while coordinating with its foundry operations to offset cost pressures from memory price increases. This effectively insulated the company from market volatility, highlighting the risk-resilience advantages of in-house chips.

Hisilicon chips used in Huawei devices also demonstrated explosive growth momentum. In the first quarter of this year, Hisilicon smartphone Soc shipments reached 16 million units, surging approximately 60% YoY. Behind this growth lie deep technological accumulation in in-house chip development, full-stack alignment with end devices, and coordinated efforts across upstream and downstream supply chains. By customizing HiSilicon chips to Huawei devices—from hardware fundamentals to software optimization—maximizing performance while controlling power consumption, and building a closed-loop “chip-device-ecosystem” barrier, while leveraging supply chain coordination to hedge against cost pressures and a stable high-end market presence, Huawei has enabled a leapfrog expansion in chip shipments.

In an environment of weak overall demand and persistently high costs, in-house chips have become not merely a symbol of technological capability, but a critical strategic asset that enables vendors to withstand market fluctuations, control core costs, and build differentiated moats. The continued rise in the share of in-house chip shipments signals a further elevation of the competitive bar in the industry.

For traditional chip design firms such as Qualcomm, MediaTek, and Unisoc, the demand pressure from their main smartphone battlefield will intensify further. Proactively diversifying into non-handset business areas such as the IoT, automotive electronics, and AIoT will become a core strategy for these companies to navigate cyclical industry risks and pursue new growth trajectories.