Tag :Display

Time :2026-5-28

In May, global monitor panel prices continued their upward trend, with the MoM price increases of mainstream specifications narrowing moderately, as the industry entered a critical period of supply and demand gaming. Driven by the combined effects of a structurally tight supply and demand landscape, continuous rises in upstream material prices, and further increased concentration in panel supply, the monitor panel market is set to maintain its price upward trajectory. However, amid persistent price hikes in the semiconductor market, prices of storage-related components in set have also kept rising. The escalating costs of non-panel components are gradually squeezing room for panel price increases. Coupled with the full halt of price gains for TV panels, brand vendors have a strong demand for narrower price increases for mainstream monitor panel specifications.

By the end of May, driven by mounting cost pressures on set and the substantial fulfillment of advance stocking needs, panel procurement demand from some brands weakened marginally, making May a pivotal period for price negotiations between supply and demand sides. Taking into account both supply and demand fundamentals as well as cost factors, #Sigmaintell forecasts that MoM price increases for mainstream monitor panels will narrow slightly in May, while mid-to-high-end panels will remain stable.

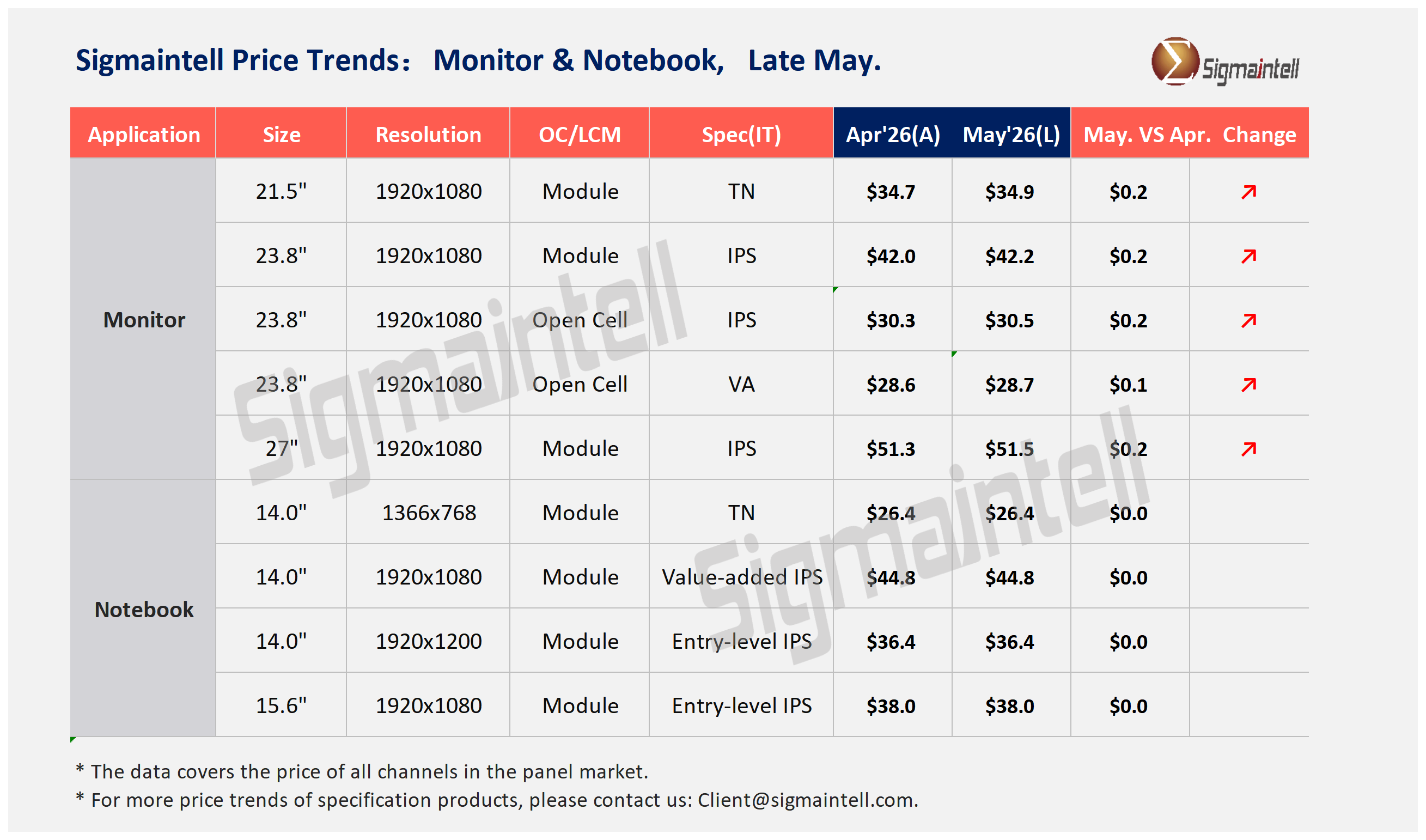

1. 21.5" FHD, mainstream IPS Open cell & LCM panel prices rose by $0.2 MoM in May;

2. 23.8" FHD, the prices of mainstream IPS Open cell & LCM panels rose by $0.2 MoM in May; the prices of mainstream VA Open cell & LCM panels rose by $0.1 MoM;

3. 27" FHD, the mainstream prices of IPS Open cell & LCM panels increased by $0.2 MoM in May; the mainstream prices of VA Open cell & LCM panels rose by $0.1 MoM;

In May, prices of mainstream-specification panels for global notebook maintained a stable trend, while mid-to-high-end specifications showed divergence. On the demand side, the continuous rise in costs of core components such as memory chips and CPUs has driven up set costs and put pressure on terminal pricing, leading to conservative expectations for the outlook of end-market demand. Although some brands have seen demand for advance stocking and promotional inventory preparation, as inventory levels rise, brands have adopted a cautious pace of stocking, resulting in overall stable yet weak demand. On the supply side, panel makers have exercised restraint in capacity release and maintained a steady production rhythm. Meanwhile, price increases in upstream materials for panels have continued to push up the MoM rise in panel BOM costs, continuously squeezing profit margins, and panel makers have a strong willingness to stabilize prices and preserve profits. Considering both supply and demand as well as cost factors, #Sigmaintell predicts that overall prices in the notebook panel market will remain stable in May, with differentiated performance across specifications: prices of low-end and mainstream specifications will remain flat MoM, while mid-to-high-end specifications will show divergent trends. Panel price performance is as follows:

1. Low-end HD TN: Prices were flat MoM in May;

2. For IPS FHD & FHD + products, the prices of mainstream 16:9 and entry-level 16:10 were flat MoM in May; the prices of mid-to-high-end panels continued to diverge.