Tag :Display

Time :2026-5-13

Core Insights:

> Global Tablet Panel Shipments in Q1 2026: A marginal YoY increase masks deep structural divergence beneath an apparently stable surface

> Declined approximately 21% YoY, with the downside cycle set to extend further

> South China tablet-like products posted YoY growth, with insensitivity to memory cost shocks and end-application spillover jointly shaping a counter-cyclical pattern

Global Tablet Panel Shipments in Q1 2026: Structural Divergence Beneath an Apparently Stable Surface

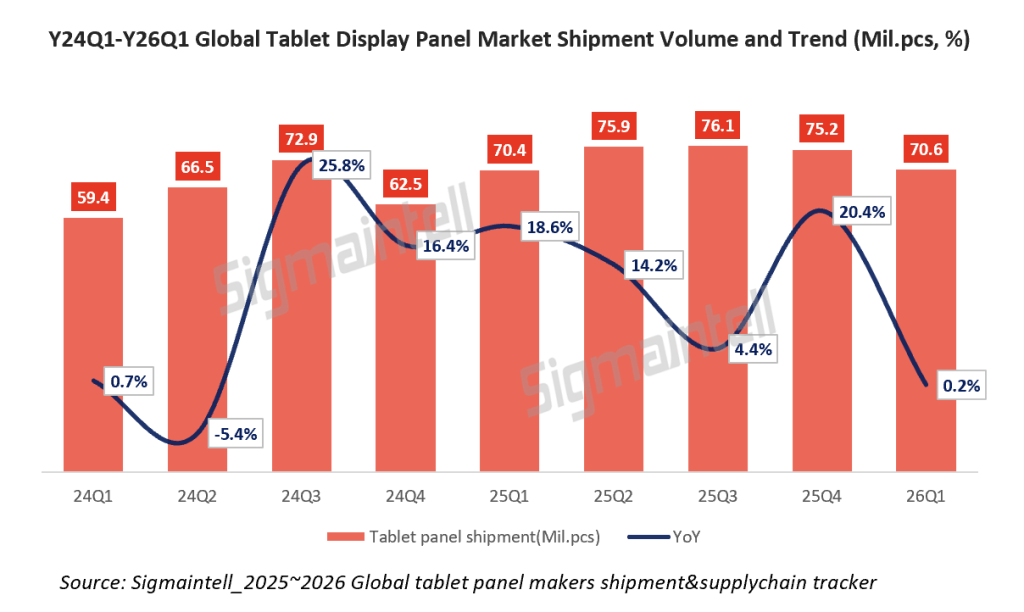

According to Sigmaintell data, global tablet panel shipments reached approximately 70.6 million units in Q1 2026, registering a slight YoY increase. However, this “stable” headline conceals significant structural distortion: on the demand side, the branded segment declined approximately 21.1% YoY, while South China demand surged approximately 25.0% YoY, adding nearly 8 million units in a single quarter. These two opposing forces offset one another, masking the true displacement of demand. This divergence is not a conventional contest between strong and weak brands; rather, it stems from the differing sensitivity of the two markets to memory cost pass-through, and the resulting reconfiguration of supply-demand structure. The “flat” Q1 2026 print should be read as the starting point of a deep divergence phase, not as a continuation of equilibrium.

Branded Segment: Q1 2026 Steep YoY Decline Has Fully Materialized; Full-Year Trajectory to Follow a “Flattened Parabola”

Weakness in the branded segment fully surfaced in Q1 2026. On one hand, Q1 is traditionally an off-season for tablets — branded retail prices remained flat, promotional activity contracted, and sell-through naturally decelerated. On the other hand, the memory cost surge that began escalating in Q4 2025 prompted brands to deliberately slow their pull-in pace; combined with concentrated channel inventory destocking and delayed new-product launches, these compounding factors drove Q1 branded panel shipments down to 30.5 million units — the lowest quarterly level since 2024.

Entering Q2, the branded segment will move into a critical phase in which cost pressure becomes overtly visible. Driven by sustained memory cost escalation, most brands have already implemented structural price hikes on both in-market models and new launches, with per-unit retail prices rising by RMB 500–1,000 across the board — a pattern of broad-based price increases spanning all tier segments. In Q2, supported by new-product release and the traditional peak season, panel shipments are expected to recover modestly QoQ, but the YoY decline is projected to persist, with seasonal recovery momentum running below historical norms.

Sigmaintell forecasts that, looking into the second half, with memory costs remaining elevated, the traditional Q3–Q4 build-up peak season will be materially compressed. Full-year branded panel demand is expected to register a double-digit YoY decline. The full-year curve is projected to take the shape of a “flattened parabola”: a steep Q1 trough, a twin-peak plateau through Q2 and Q3, and a moderate pullback in Q4.

South China Tablet-Like Products: Memory-Cost Immunity and End-Application Spillover Shape a Counter-Cyclical Pattern

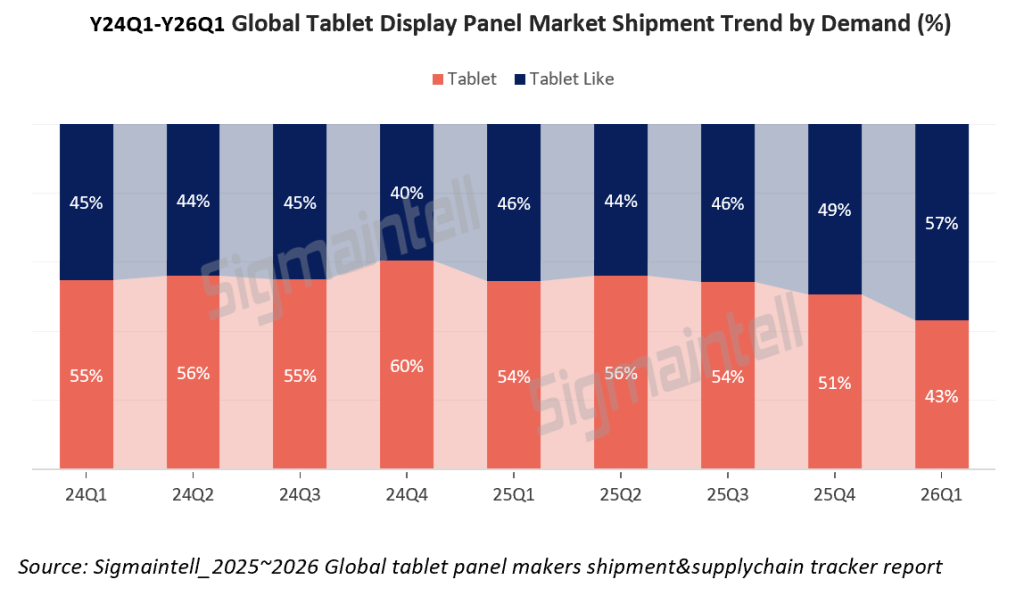

In sharp contrast to the branded segment, demand for South China tablet-like products has not been materially affected by memory price inflation. Q1 build-out remained robust, with this segment's share of total tablet panel shipments reaching 57% — an 11-percentage-point YoY increase. According to Sigmaintell research, this counter-cyclical performance is not coincidental; three underlying drivers are at work:

(1) Low sensitivity to memory cost shocks

Branded tablets rely heavily on DRAM and NAND Flash, and the specifications they use sit squarely within the mainstream impact range of this round of price hikes. Over the past year, memory prices have risen approximately 4x–5x cumulatively, lifting the memory share of branded tablet BOM from a previous 15%–20% to 50%–70%. Memory has now surpassed both the panel and the SoC to become the single largest cost line item in a branded tablet's BOM, exerting structural pressure that branded OEMs cannot absorb on their own.

Tablet-like products (POS ordering terminals, automotive secondary displays, industrial panels, public information displays, retail interactive terminals, etc.) typically employ “legacy-generation memory” such as DDR3/DDR4 paired with eMMC; some applications operate without dedicated DRAM altogether. Combined with per-unit memory content that is already far lower than branded tablets, and with broader sourcing channels — module houses, white-box vendors, and reclaimed-die supply — the overall BOM exposure to memory volatility is far smaller than in branded tablets.

(2) Supply chain flexibility to “downgrade specs to safeguard delivery”

The tablet-like supply chain has the elasticity to “downgrade specifications to safeguard delivery,” offsetting cost increases by flexibly adjusting memory configurations. Branded tablets, by contrast, find it difficult to downgrade given product-positioning and user-experience constraints. This supply-chain-side flexibility further amplifies the gap in cost sensitivity between the two segments.

(3) Continued diversification and expansion of end-applications

Diversification of tablet-like applications continues to accelerate. Innovative use cases, automotive aftermarket, industrial control, public information displays, and retail interactive terminals are advancing in parallel, with tablet-like products evolving from “an extension of consumer tablets” into an independent mid-size touch-display interaction ecosystem. Demand here is driven primarily by B2B project orders and new-category dividends — making it weakly cyclical or even counter-cyclical, and largely insulated from consumer-side price disturbances.

Looking into 1H 2026, tablet-like demand is expected to maintain its strong momentum, standing in sharp contrast to the contraction in the branded segment. However, whether this segment can sustain elevated levels into 2H carries meaningful uncertainty: on one hand, prolonged memory price inflation will eventually transmit at the margin into the tablet-like supply chain; on the other hand, the B2B project-driven portion of tablet-like demand is inherently pulse-like in its release pattern, and combined with the high base effect set by 1H, 2H cadence is likely to exhibit volatility.

Conclusion and Outlook: Amid Intensifying Divergence, the Tablet Industry Enters a Phase of Structural Reconfiguration in 2026

Taken together, the global tablet panel market in Q1 2026 has shifted from a phase of “aggregate volume growth” into a critical phase of “structural reconfiguration.” In Sigmaintell's view, the apparently flat YoY headline conceals a stark divergence between the branded segment and South China demand; and as the core driver of this divergence, the asymmetric impact of memory cost inflation will continue to play out over the remaining three quarters of 2026, shaping the industry's full-year trajectory. From a cadence perspective, 1H 2026 will exhibit a dual-track pattern of “visible pressure on brands, robust South China demand acting as an offset,” with overall shipments likely to remain broadly stable. Moving into 2H, the branded segment will enter a phase of deeper release of memory-cost pressure, while the sustainability of South China's elevated levels remains highly uncertain — collectively pointing to a risk of phased weakening for the market as a whole.