Tag :Display

Time :2026-5-26

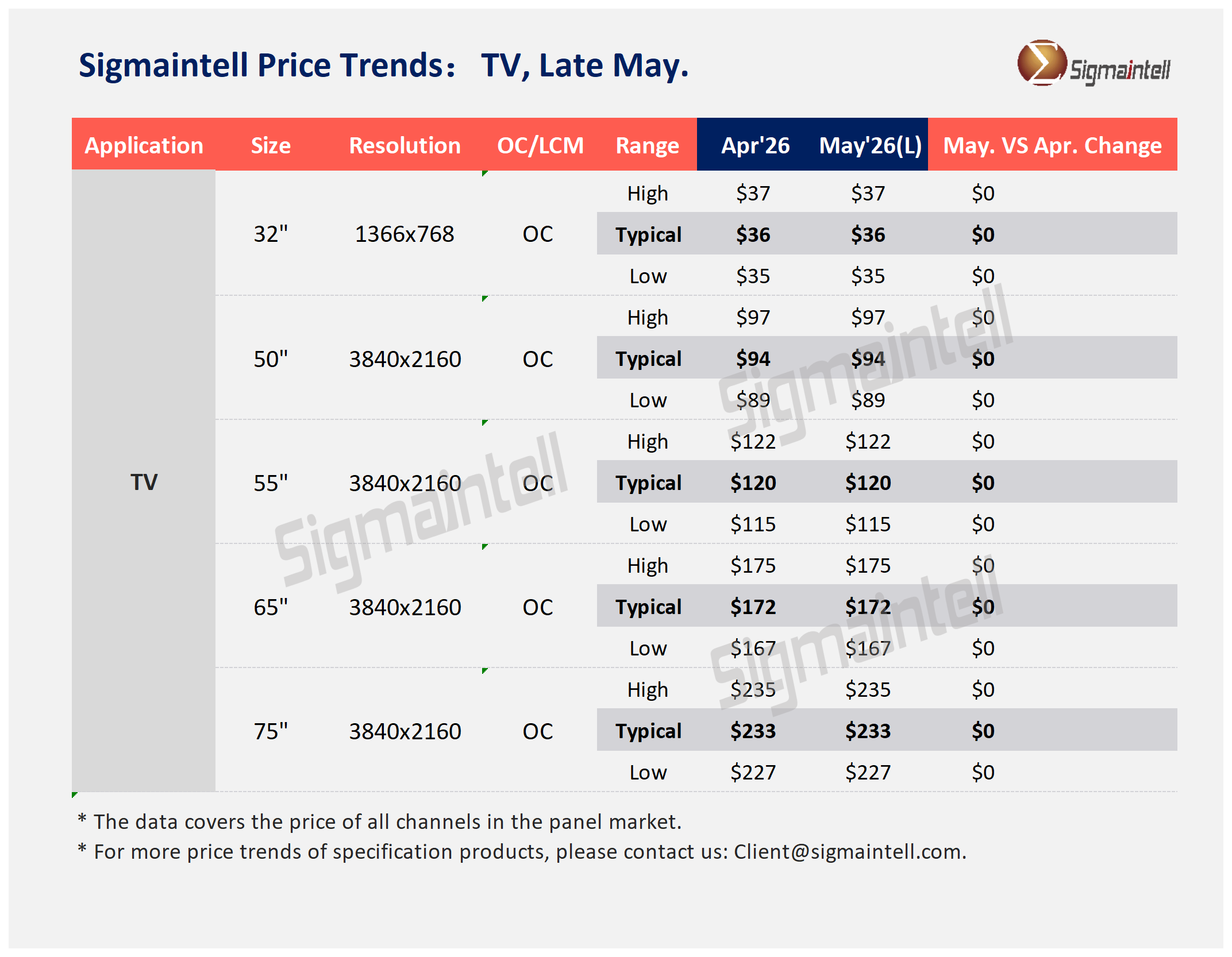

As of May, the pace of demand-side adjustments has slowed, with the global TV panel market maintaining a static equilibrium. From the perspective of panel demand, following the conclusion of both sports event-related stocking and the first-half promotion inventory buildup, brand vendors have largely completed deep adjustments to their second-quarter procurement strategies, resulting in a sequential softening of overall stocking momentum. Rising costs of memory components have exerted pressure on ODMs and second-tier brands, emerging as a key short-term risk to panel demand. Against this backdrop, demand dynamics across sizes have diverged: demand for small-size panels has cooled markedly, while large-size products remain resilient, supported by major brands. In response to these demand shifts, panel suppliers have adjusted flexibly. Specifically, leading panel makers implemented production controls in May while concurrently reducing capacity allocation to small- and medium-size segments, thereby mitigating the risk of supply-demand looseness across sizes. Overall, moderate adjustments on both supply and demand sides have kept short-term panel prices largely stable. The price trends by size are outlined below:

32”: Demand has cooled noticeably, prompting panel makers to curb capacity; prices are expected to stabilize in May.

50”: Capacity on G8.6 lines faces pressure from ultra-large-size production; average prices are forecast to remain stable from May to June.

55”: Stable demand and concentrated supply support price stability in May

Large sizes: Robust brand procurement demand, combined with strong production controls at G10.5 lines, reinforces price stability in May.