Tag :Display

Time :2026-5-18

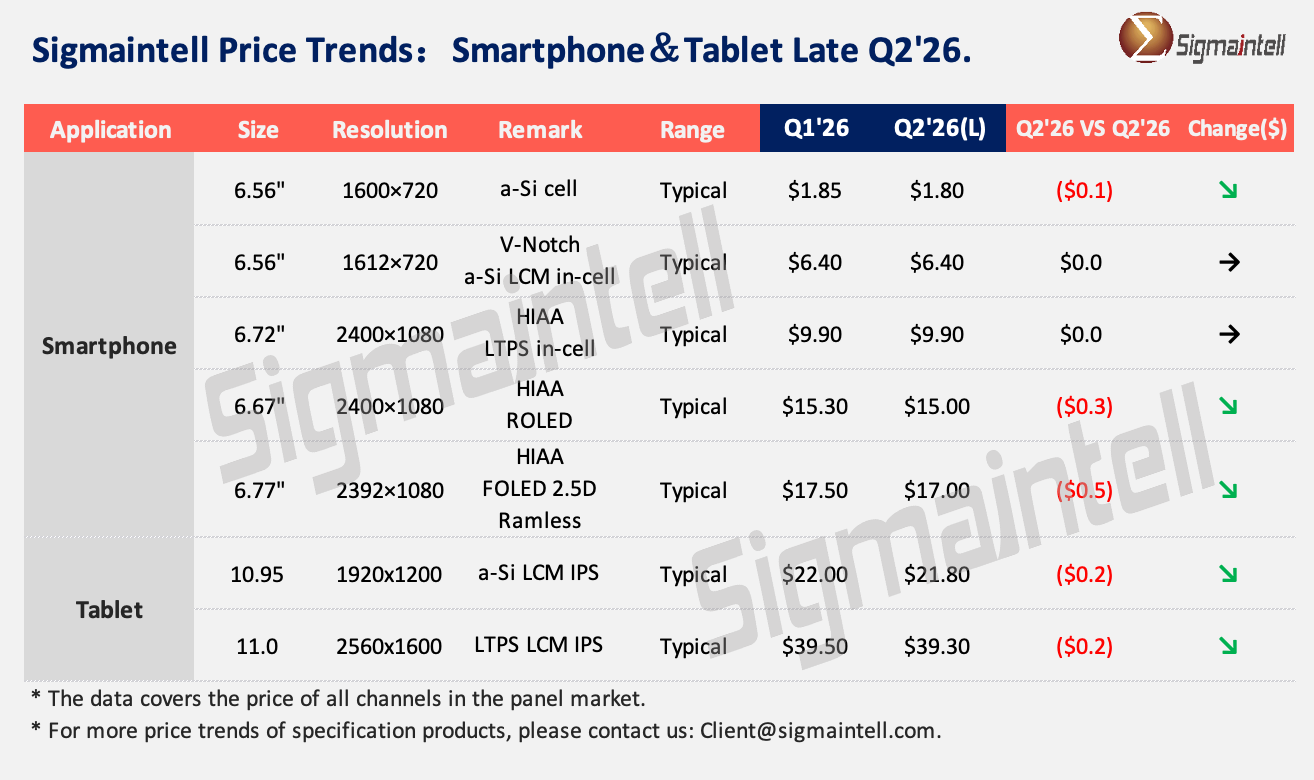

In Q2 2026, the global smartphone display panel market continued to grapple with sluggish demand, maintaining an oversupplied and loose overall market landscape. The industry faced tough headwinds amid high costs and weak demand. While overall panel prices remained stable, divergent trends emerged significantly across different technology segments. Detailed analysis is as follows:

a‑Si LCD: Driven by advance stocking by end brands to offset rising upstream costs in Q1, shipments posted a mild year‑on‑year increase. However, demand showed signs of decline in Q2. Coupled with persistent cost hikes for driver ICs and module materials, module makers faced substantial profit pressure. End market demand stayed muted, and brand clients maintained strict order control. Supported by supply‑demand dynamics and stable bulk raw material prices, panel prices held steady; nevertheless, rising costs pose upside risks to prices in the second half of the year.

LTPS LCD: Demand for LTPS LCD panels remained weak in Q2. Its market footprint continued to shrink amid competition from cost‑effective a‑Si LCDs and mid‑to‑low‑end FOLEDs, with no momentum for recovery as it gradually exited mainstream supply chains. Restrained by mounting costs and shrinking demand, panel prices stayed flat.

ROLED: Rigid OLED panels faced ongoing demand contraction and accelerated substitution. Aggressive pricing strategies for flexible OLED panels further directly pressured ROLEDs, leading to continued price declines in Q2.

FOLED: The FOLED market featured loose supply‑demand balance and cutthroat competition, intensifying operational pressures for domestic panel makers. Driven by weak demand and capacity competition, panel prices kept falling and remained under heavy pressure in Q2.

Against the backdrop of continuous price hikes for memory chips, end brands have faced sharply rising profit pressure, passing cost burdens upstream to core component supply chains such as display panels. Nevertheless, for the panel supply chain, prices of some raw materials remain on an upward trajectory, putting overall cost pressure on panel makers. Meanwhile, retail prices of finished tablets were generally raised in Q2, which in turn slowed market demand momentum. Against this backdrop, panel makers are seeking a balance between utilization rate and profitability. Sigmaintell Forecasts Price Trends by Technology Segment:

a-Si LCD: Overall supply demand balance remains relatively stable. Coupled with panel cost pressures, the downward price trend has narrowed.

LTPS LCD: Affected by softening demand, LTPS product prices have seen minor adjustments this year. Panel prices are expected to post a slight decline in Q2.