Tag :Display

Time :2026-5-25

Core Insights:

> Accelerated restructuring of the global supply chain and upgraded strategy for independent control of OLED materials

> Demand structure iteration: Coexistence of total volume growth and slowing growth; short-term pressure does not alter long-term resilience

> Global scale exceeds 16.3 billion yuan with moderate growth slowdown and accelerated high-quality development

> Domestic makers lead the global OLED intermediate materials market with simultaneous growth in share and value

> Outlook: Localization enters full-scale implementation phase; AI and security jointly build a new future for the display industry

Accelerated Restructuring of Global Supply Chain and Upgraded Independent Control Strategy for OLED Materials

The global technological competition landscape continues to evolve, with trade controls, supply chain security and technical barriers profoundly impacting the high-end display industry chain. For a long time, core OLED materials have been highly dependent on imports; overseas enterprises have dominated relying on technological, patent and ecological advantages, becoming a key constraint on the independent control of the display industry.

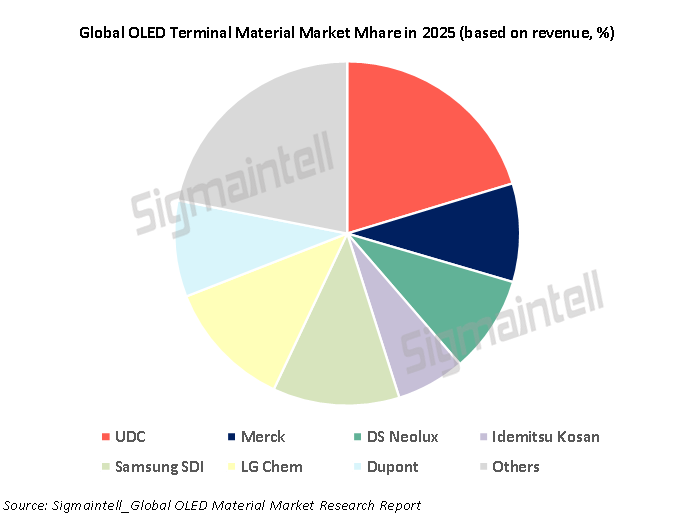

From the perspective of global competition, OLED terminal materials are still dominated by leading overseas enterprises. UDC, Merck, Samsung SDI, LG Chem, DS Neolux, Idemitsu Kosan, DuPont and other companies maintain leadership in high-end fields such as luminescent materials and transport materials, with high industry concentration. Domestic material enterprises have continuously increased R&D investment and capacity construction, achieved breakthroughs in segmented tracks, and steadily improved overall competitiveness; their future growth potential and development momentum are significantly better than those of traditional advantageous regions.

Demand Structure Iteration: Coexistence of Volume Growth and Slowing Growth; Short-term Pressure Does Not Change Long-term Resilience

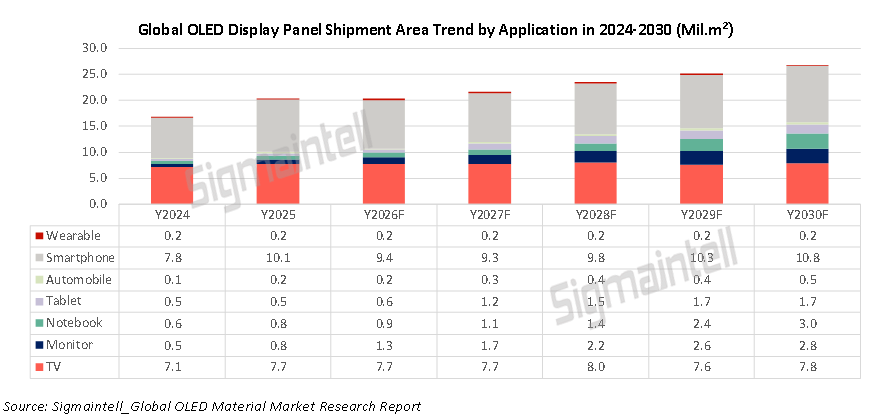

According to Sigmaintell data, the global OLED panel market maintained growth in 2025, with shipment area reaching 20.4 million square meters, a YoY increase of 22%, providing demand support for upstream materials. The industry has shifted from a high-speed outbreak period to a stage of structural growth. In 2025, the OLED market featured stable mobile phone demand, explosive IT growth and rapid automotive growth.

Entering 2026, with the mass production of G8.6 OLED production lines, cost reduction will further accelerate penetration in the medium-size application. However, affected by factors such as rising storage chip prices squeezing end costs, prolonged replacement cycles of consumer electronics, concentrated release of panel capacity and channel inventory destocking, end brands have lowered shipment plans, and industry growth will face periodic pressure. The global OLED panel shipment area is expected to decline slightly year-on-year, and major panel makers will adjust utilization rates and reduce upstream material procurement accordingly.

In the medium and long term, driven by medium-size application demand such as IT and automotive, the global OLED panel shipment area will maintain a CAGR of approximately 5.6% from 2025 to 2030, and is expected to reach 26.8 million square meters in 2030; the industry remains in a healthy upward cycle. The contribution of Domestic OLED panel shipments continues to rise, from about 5.3 million square meters in 2025 to 7.8 million square meters in 2030.

Global Scale Exceeds 16.3 Billion Yuan, Growth Moderates, High-quality Development Accelerates

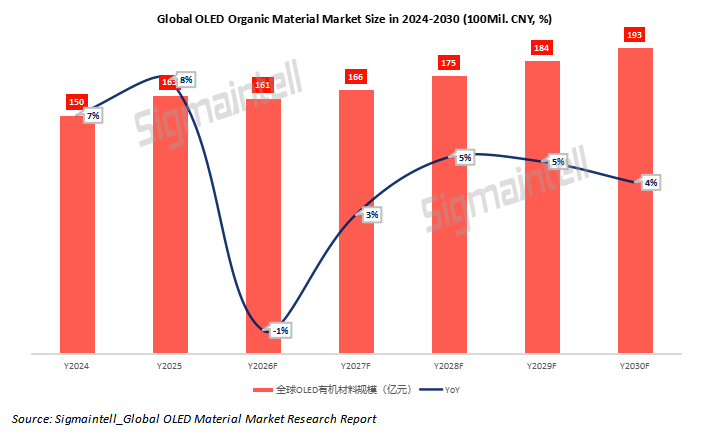

According to Sigmaintell data, the global OLED organic materials market size was about 16.3 billion yuan in 2025, a year-on-year increase of 8%. Among them, the Domestic OLED organic materials market size was about 6.2 billion yuan in 2025, maintaining expansion supported by deepened terminal penetration and released panel capacity, but growth has returned to rationality affected by intensified price competition and demand structure adjustment. Despite slower growth, the market base continues to expand, and the industry has entered a new stage of steady growth.

In 2026, affected by shrinking panel shipments and intensified industry competition, the OLED organic materials market will continue to face dual pressure from volume and price, with short-term pressure on revenue growth, and the industry will enter a phased adjustment cycle. However, it will maintain steady growth in the medium and long term. The global OLED organic materials market size is expected to exceed 19.3 billion yuan by 2030, of which the Domestic market will reach 8.4 billion yuan.

Domestic Makers Lead Global OLED Intermediate Materials Market, Share and Value Rise Simultaneously

The OLED material industry chain is divided into three links: basic chemicals, intermediate materials, and terminal materials. Terminal materials have high barriers and are patent-intensive, while intermediate materials have become the main track for the first breakthrough in domestic substitution.

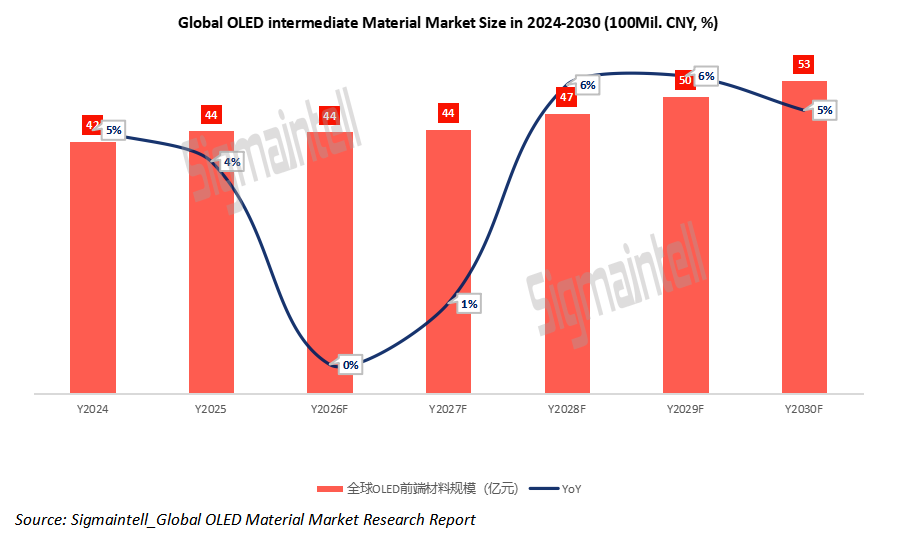

Affected by intensified domestic competition and transmission of panel price cuts, the global OLED intermediate materials market size was 4.4 billion yuan in 2025, a slight year-on-year increase of 4%. Sigmaintell predicts that intermediate materials will continue to face pressure in 2026, and the contraction and price pressure at the panel end will further transmit to the intermediate materials segment. In 2027, as global OLED panel demand gradually recovers, inventory cycles clear, and new applications such as IT and automotive continue to expand, market demand will resume growth synchronously. The global OLED intermediate materials market size is expected to reach 5.3 billion yuan by 2030.

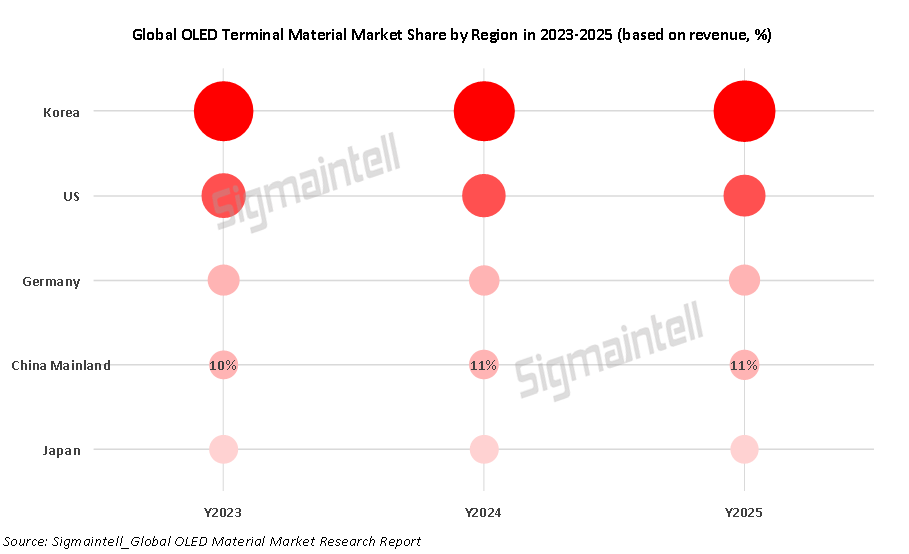

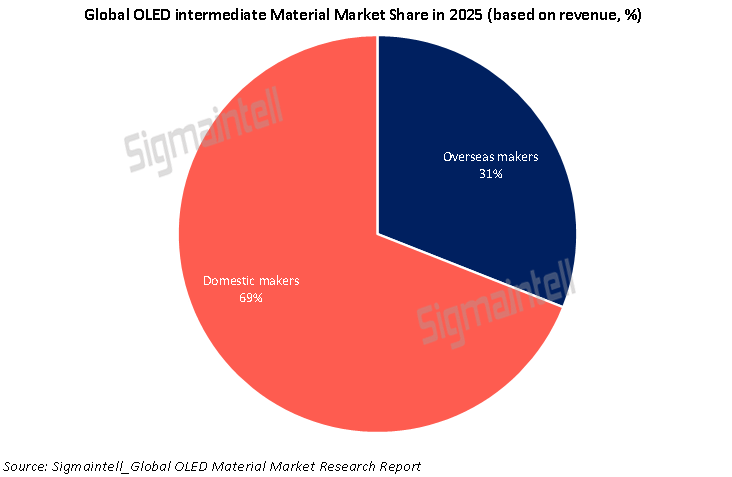

Relying on cost, delivery and supply chain advantages, Domestic makers have become the core global supply force. Gem Chemical, Xi’an Manareco, Puyang Huicheng and others have steadily entered the supply chains of global leaders such as Samsung SDI, Idemitsu Chemical, LG Chem and UDC. In 2025, Domestic makers accounted for 69% of the global OLED intermediate materials market, jointly forming the world's major supply pattern.

At present, the added value of intermediate materials is relatively limited added value, but leading enterprises are accelerating the upgrade to high-purity, customized and high-barrier products. Meanwhile, the advantages of intermediate materials will provide technical, financial and ecological support for the breakthrough of end materials, promoting the overall OLED material industry in China to move towards a world-class level.

Outlook: Localization Enters Full Implementation Period, AI and Security Build a New Future for the Display Industry

2025 is a pivotal year for OLED material localization shifting from verification and introduction to large-scale volume production. Against the backdrop of AI technological upgrading, supply chain restructuring and changing international trade environment, Domestic material enterprises have accelerated the pace of substitution relying on advantages in technology, cost, response speed and industrial chain collaboration.

Sigmaintell believes that in the future, Domestic OLED materials will gradually upgrade their industrial status from "optional" to "core", promoting the leap from supporting to leading in key materials for new displays. Driven by AI innovation and industrial security, Domestic OLED material industry will continue to improve its ecosystem and enhance competitiveness, helping the display industry occupy a more important position in the global industrial landscape.