Tag :Semiconductor

Time :2026-6-18

In 2026Q2, the global Memory market continued to be deeply immersed in the super - storage cycle environment. Throughout the quarter, the market remained in a state of supply - demand shortage, and the characteristic of price differentiation was extremely prominent. In Q2, with the mass production and shipment of the new - generation GPU, the demand for HBM4 and LPDDR increased, and the demand for eSSD in servers also increased significantly. As a result, the supply shortage of DRAM and NAND used in consumer electronics persisted, and prices continued to rise substantially.

DRAM: Obvious price differentiation, and the upward trend gradually slows down

In 2026Q2, the price of DRAM continued to rise.

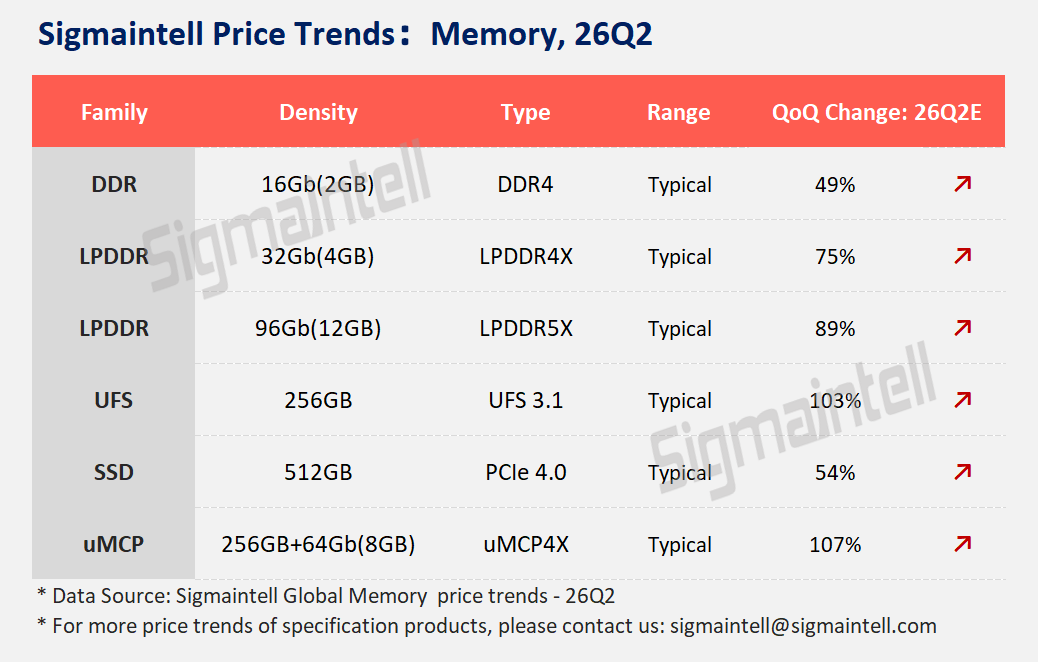

Consumer - electronics DRAM: The contract prices of consumer - electronics DRAM mainly including LPDDR4X/LPDDR5X still maintained a strong upward trend. On the one hand, LPDDR is the main DRAM for the new - generation server GPU architecture. The competition for supply has prompted storage original manufacturers to increase the price increase for consumer - electronics customers, and some consumer - electronics customers took the lead in accepting the price increase, which promoted the establishment of a significant price increase. According to the data of Sigmaintell, the price of 4GB LPDDR4X in the second quarter increased by 75% compared with the first quarter. However, due to the rise in memory prices having a significant impact on the demand in the consumer - electronics market, and consumer - electronics terminals actually feeling the cost pressure, some brand customers began to gradually reduce the order quantity, which may suppress the price increase of consumer - end DRAM in 26H2.

General - purpose server DRAM: Among consumer products, the price increase of general - purpose server DRAM led the way. Its channel inventory has been maintained at a low level, only about 2 - 3 weeks, and cloud vendors have been continuously replenishing inventory, which has kept the price of this product rising following the overall industry trend.

AI server / HBM: As a core product indispensable in the AI field, the production capacity of HBM is preferentially guaranteed by manufacturers for supply. Its price has been locked through an annual contract and remained stable throughout 2026. Currently, the supply - demand contradiction of HBM is extremely acute, and wafer resources are continuously concentrated on it.

Looking at both the supply and demand sides and the long - term trend, the DRAM market showed an upward trend in 2026Q2, but the increase was divergent. On the demand side, the strong demand for AI servers has increased the demand for high - bandwidth memory, while the demand in the consumer - electronics field is polarized. The demand for mid - to - high - end products is rigid due to performance and experience requirements, while the demand for low - end products is suppressed by the rising price due to price sensitivity.

On the supply side, the mass production of high - value - added memory products, their complex processes increase production difficulty and consume more wafer production capacity. Moreover, the original manufacturers have low inventory, limited capacity expansion ability, and preferentially guarantee AI customers, resulting in the squeezing of consumer - end DRAM production capacity and supply shortage. Overall, in this quarter, the supply - demand shortage of DRAM was severe, the price continued to rise but with obvious differentiation.

NAND: The upward trend continues, and the supply gap widens

It is expected that in the second quarter of 2026, the NAND flash memory market will continue the previous upward trend, and the price increase will become more rapid. According to the data of Sigmaintell, the price of SSD in the second quarter of 2026 increased by about 50% compared with the first quarter, and the quarterly increase of mobile - end UFS expanded to about 100% compared with the previous quarter.

In the field of server / AI eSSD, with the significant increase in the storage capacity of AI clusters and agent servers, the server heterogeneous technology architecture has strengthened the demand for the performance and capacity of dynamic data storage, thus greatly stimulating the growth of data - storage demand. Enterprise - level NAND, as the key storage medium to meet such demands, has shown extremely strong demand growth. Regardless of how the market price fluctuates, the procurement demand for enterprise - level NAND has always been high, driving its price to rise substantially.

In contrast, in the NAND market of consumer electronics such as PCs / smartphones, although the price has also increased, there are complex situations hidden behind it. The price increase in the consumer - electronics NAND market is driven by the squeeze of supply. However, due to the still - growing demand for local storage and the supply - side contraction of low - end NAND supply (such as small - capacity eMMC), it is difficult for the demand for consumer - end storage NAND to decline.

Overall, in 2026Q2, the NAND flash memory market was driven by the demand of server / AI eSSD. The rigid demand supported the strong upward movement of prices. In the NAND market of PCs / smartphones, although the price increased, due to factors such as supply squeeze and high prices suppressing demand, there is pressure for the future price increase to converge. This not only reflects the profound reshaping of the NAND market demand structure by AI technology but also highlights the different trends of different market segments under the change of supply - demand relationships, indicating that the market is in a process of dynamic adjustment and balance.