Tag :Display

Time :2026-6-29

Core Insights:

>Structural growth momentum is significant, OLED has become a definitive market direction: Against the backdrop of slowing overall growth momentum in the global laptop panel market, OLED panels, especially those targeting large-screen (15-inch and above) mainstream and high-performance scenarios, are showing shipment growth rates that outperform the broader market.

>The "technology anchoring" effect is prominent in the era of stock competition: As the market transitions from incremental sharing to stock competition, technological generation gaps have become a core weapon for brands to build product moats and compete for high-end market share. With its image quality performance and form factor advantages, OLED is becoming a key "technology anchor point" in the large-screen thin-and-light and gaming laptop markets.

>Capacity and technology roadmap competition will determine the long-term landscape; multiple OLED technology routes are key shaping forces for laptop panel technology.

I. From "Small" to "Large": The Counter-Cyclical Expansion of the Global OLED Laptop Panel Market Amid Demand Challenges

The global laptop market is currently facing multiple challenges: slowing end-user demand growth, high costs of memory components, and supply chain uncertainties caused by CPU platform transitions have collectively led the overall market to shift rapidly from a quarterly boom driven by "preventive stockpiling" to a cautious cycle dominated by inventory digestion and wait-and-see. Against this macro backdrop, panels based on different technology routes are showing distinctly different market resilience.

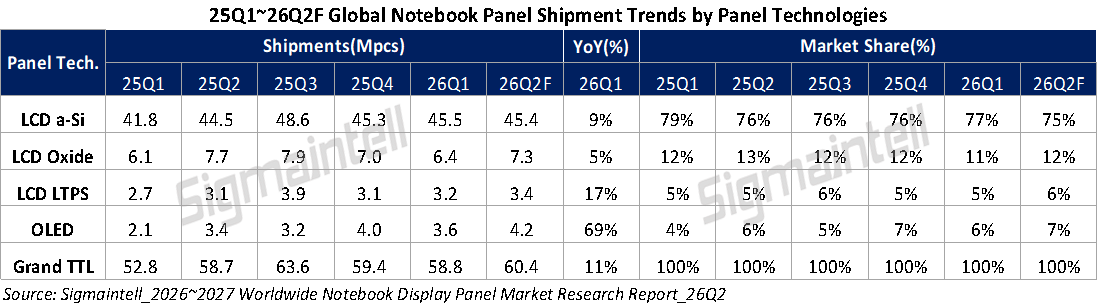

According to Sigmaintell's shipment tracking data for the global laptop panel market segmented by technology, a-Si LCD, as the fundamental base, has hit a growth bottleneck. However, OLED panel shipments achieved a significant leap from 2.1 million units in Q1 2025 to 3.6 million units in Q1 2026, and are expected to continue increasing to 4.2 million units in Q2, leading the growth rate among all technology paths.

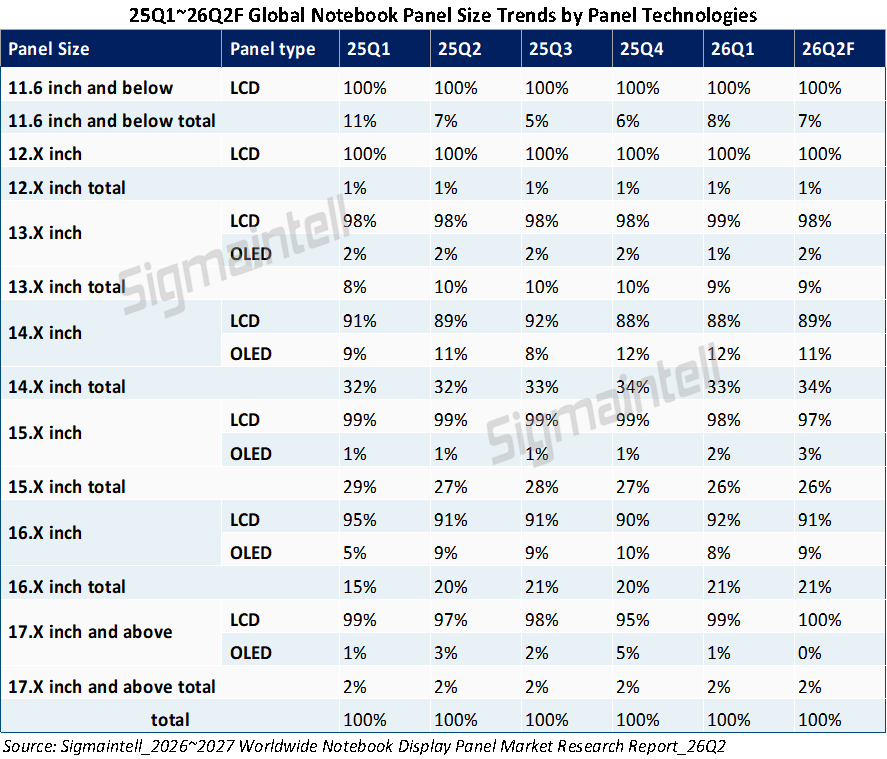

More crucially, this growth exhibits a clear shift from "small" to "large": the growth momentum has rapidly expanded from the initial 14-inch and below products in the early OLED laptop market to 15.X-inch and above large-size products. The 15-inch and above large-screen laptop market has long accounted for about 50% of the global laptop panel market share, making it a very important core market segment for this category. Furthermore, the large-screen laptop product line is complete, comprehensively covering diverse user groups from entry-level to flagship, from basic office work to mainstream gaming, and high-end creation and professional users. Therefore, the product specifications in the large-screen laptop market are extremely rich, and the demand for display technology upgrades holds significant potential. With the increased R&D investment in large-screen laptop technology by rigid FMM OLED in recent years, OLED products in the 15-inch to 16-inch range have gradually become more abundant, steadily opening up new growth poles.

Taking the 16.X-inch market as an example, its OLED penetration rate began to increase significantly from 5.1% in 25Q1, with a clear trendline pointing towards a higher share. The 15.X-inch market has also seen a noticeable increase in OLED penetration this year. This is not an accidental industry fluctuation but the inevitable result of the alignment between the performance upgrade demands of large-screen laptop products and panel manufacturers' dual-line product strategy of "mainstreaming + gaming." This indicates that during overall market pressure, sub-markets driven by technological innovation possess stronger anti-cyclical capabilities, and OLED has become the definitive technological direction in this field.

II. Deconstructing Technology Paths: How Three Major OLED Processes Support the Technological Advancement of Large-Screen Laptops

Within OLED, different manufacturing processes have varying degrees of suitability for meeting the diverse and specification-rich demands of large-screen laptops, collectively forming a complete technology matrix that caters to needs from mainstream to flagship.

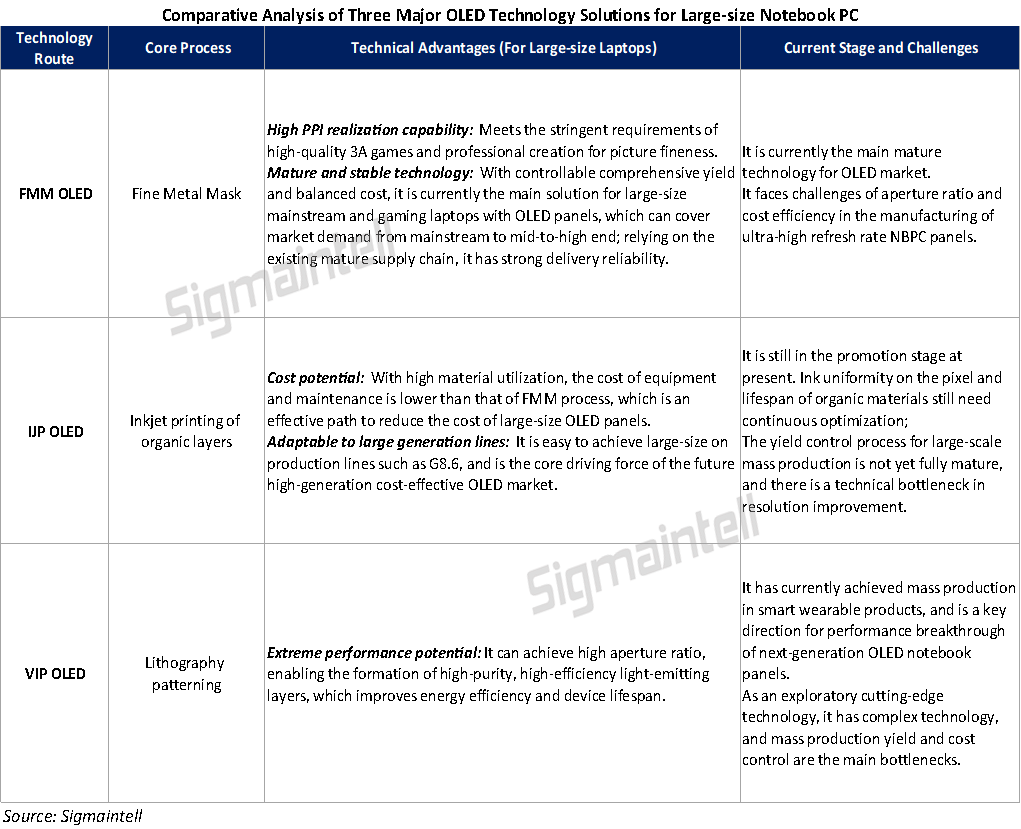

1. FMM OLED: The Current Mainstream Mature Solution for the OLED Laptop Market

As the most widely used technology path in large-screen OLED laptops currently, FMM OLED, with fine metal mask as its core process, has clear advantages for large-screen laptop products:

First, it possesses excellent capability for achieving high PPI, meeting the stringent requirements for image detail in high-quality 3A games and professional creation, and adapting to the high-resolution demands of large-screen laptops. Second, it has high technological maturity. ROLED, the foundation of current FMM OLED laptop products, boasts high mass production yield, and rich color calibration experience, making it the most stable choice for the mass market. The shortcomings of FMM OLED are also relatively apparent. It has entered a period of application maturity, with limited room for further performance improvement. In the manufacturing of ultra-high refresh rate panels, there is always a contradiction between increasing aperture ratio and cost control, making it difficult to simultaneously meet the dual requirements for higher specifications in both parameters and cost for more advanced products.

2. IJP OLED (Inkjet Printing OLED): The Core Driving Force for the Future Popularization of Large-Screen OLED Laptop Displays

The inkjet route, with inkjet printing of organic layers as its core process, possesses inherent industrialization advantages for large-screen laptops: On one hand, its cost potential is outstanding. The material utilization rate of the process is far higher than the traditional FMM route, making it the optimal path for currently reducing the cost of large-screen OLED panels, potentially addressing the core pain point of OLED laptop pricing. On the other hand, it is naturally suitable for high-generation production lines, possessing the potential for producing large-size panels on high-generation lines like G8.6, which can further amortize panel production costs. It is the core driver for future growth in the high-generation cost-effective OLED market. Currently, this technology is on the verge of mass production but remains in the critical phase of mass production maturation. Issues such as insufficient printing precision, poor film uniformity, relatively low luminous efficiency, and energy consumption performance needing optimization still need to be resolved through gradual process refinement during the production ramp-up phase.

3. VIP OLED (Visionox Intelligent Pixelation): The Breakthrough Direction for Flagship Performance

VIP OLED, with lithographic patterning as its core process, is a cutting-edge route for enhancing the performance of large-screen OLED laptop displays: Its technological advantages are concentrated in performance upgrades. The lithography process can form high-purity, high-efficiency light-emitting layers, which can directly improve panel brightness, energy efficiency, and extend device lifespan, while also bringing significant gains to the large-screen HDR experience. Simultaneously, its process characteristics are expected to support the stability of ultra-high-frequency PWM dimming, meeting the eye-care demands of high-end users and aligning with the current focus on visual health in high-end laptops. Currently, VIP OLED has achieved mass production in smart wearable products, but its application in large-screen laptops still faces many challenges: it belongs to exploratory frontier technology, with high overall process complexity. Improving mass production yield and cost control are the most critical breakthrough directions.

Judging from the plans of leading manufacturers in the above three technology routes regarding high-generation OLED NB products, increasing investment in the large-screen OLED laptop market is also a clear technological strategy. Overall, the three paths form a gradient-complementary technology matrix, jointly promoting the technological upgrade and market expansion of large-screen OLED laptop display solutions.

III. Dual Drivers of Technology Iteration and Demand Upgrade: The Long-Term Growth Logic for OLED in the Global Laptop Panel Market is Clear

From the industry environment perspective, rising memory costs have indeed brought some cost pressure, but they have not affected the penetration of OLED in the global laptop panel market. This year, while storage costs for mainstream large-screen laptops have increased, for creative and gaming users willing to pay a premium, the display experience improvement brought by OLED remains sufficiently attractive, and demand growth in the high-end market has not been affected. For mid-range price segments, OEMs are steadily promoting OLED adoption by offsetting some cost pressures through supply chain optimization, and overall industry penetration is progressing according to schedule.

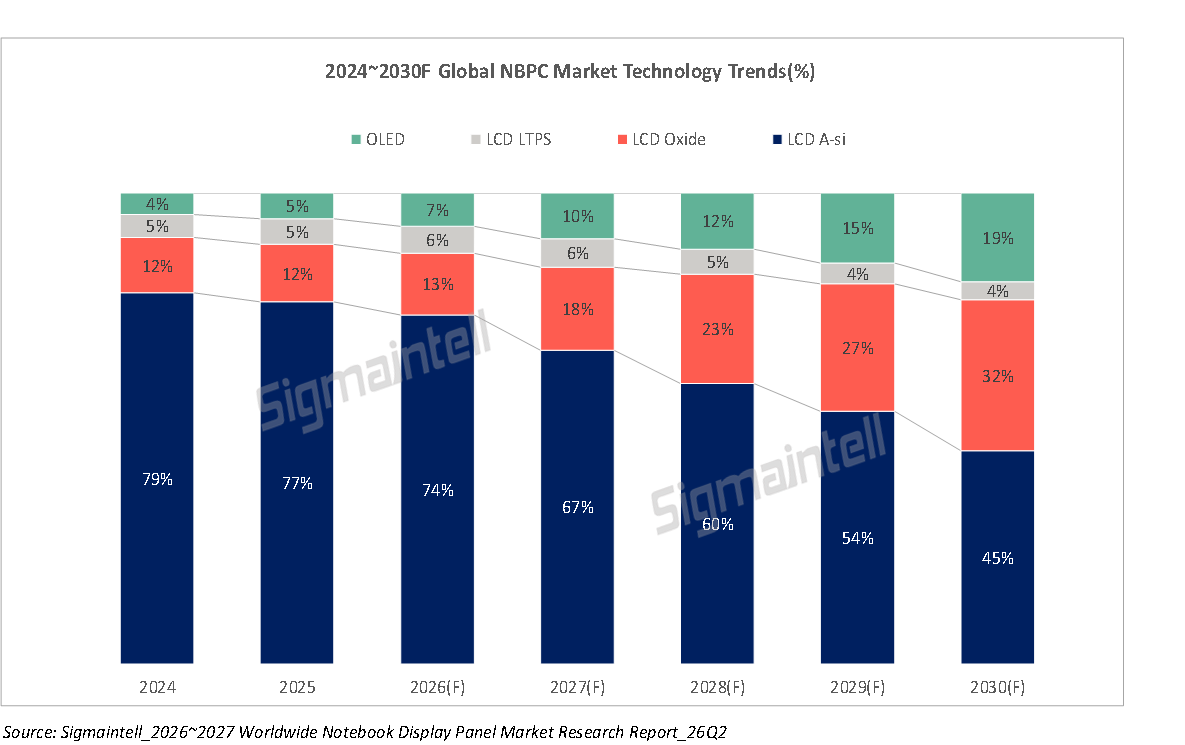

Currently, large-screen OLED still has room for optimization in areas such as lifespan, brightness, power consumption, and supply chain singularization. These issues are expected to gradually improve with the release of high-generation OLED capacity and technological iteration across multiple technology routes. In the long term, the growth momentum for large-screen OLED laptops is very clear: On the consumer side, the popularization of demands like content creation and 3A gaming drives continuous improvement in user requirements for screen quality. OLED's inherent advantages of high contrast ratio, wide color gamut, and extremely fast response are highly aligned with the direction of PC users' screen demand upgrades, and market recognition is continuously increasing. On the supply side, as the scale effect of high-generation OLED production lines further narrows the cost gap, it will drive OLED to cover the entire PC market from mainstream to flagship price segments. Coupled with the development of emerging scenarios like VR/AR external displays and foldable/rollable form factors, OLED's flexible and low-latency characteristics will open up more imaginative growth space in the global IT market. Sigmaintell forecasts that by 2030, the penetration rate of OLED technology in the global laptop panel market is expected to climb to 19%.

Overall, OLED technology is currently in a benign development stage of steadily penetrating from small-screen to large-screen laptop markets. Panel manufacturers can continue to rely on a gradient technology layout, consolidating their advantageous position in the mid-to-high-end market on one hand, and accelerating the mass production maturity of new processes on the other, gradually releasing cost and performance advantages. This will enable them to continuously promote the growth of the OLED IT market and lead the ongoing upgrade of laptop product display experiences.