Tag :AI, Semiconductor

Time :2026-5-11

In early May, the CEO of global leading AI company Anthropic publicly announced that the company's revenue and usage increased 80-fold in the first quarter on an annualized basis. This growth rate significantly exceeded the company's previously set target of 10-fold growth and was accompanied by mention of severe computational power shortages currently faced. This figure starkly highlights the current magnitude of global AI computational demand and the status of storage requirements.

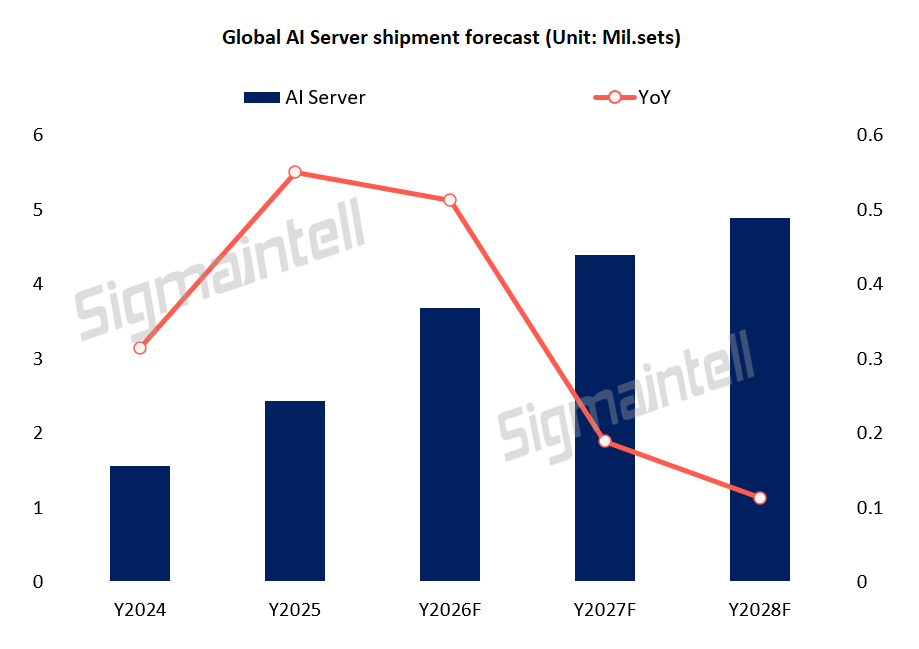

According to the latest forecasts from Sigmaintell, global AI server shipments are expected to reach 3.7 million units in 2026, a year-on-year increase of 51.3%. The growth of AI servers is reflected not only in the expansion of shipment volume but also in the increase in storage capacity per unit. Compared to traditional servers that primarily rely on homogeneous computing with multiple CPUs, resulting in low computational density and small memory capacity, generative AI large models—with their growing parameters, longer context lengths, and explosion of multimodal data—make heterogeneous computing the core technical path for AI servers. Taking NVIDIA's Blackwell and Vera Rubin architectures as examples, their designs enhance deep heterogeneous collaboration capabilities, using high-speed interconnects like NVL to link CPUs, GPUs, HBM, and DDR memory, achieving integrated coordination of computation, storage, and scheduling. Similarly, Google's Gemini computational clusters adopt a CPU+TPU heterogeneous architecture. Within heterogeneous architectures, high-frequency interaction among multiple chips and real-time data flow of Token data require both large-capacity DDR as system memory and high-bandwidth HBM for instantaneous computational throughput. Consequently, to meet the demands of intensive model inference, the DRAM capacity equipped in AI servers shows a significant multiplicative increase compared to traditional servers. Additionally, HBM, as a specialized high-bandwidth memory chip, continues to consume substantial storage supply.

Benefiting from this, Sigmaintell assesses that AI servers will have a revolutionary impact on the demand structure of the DRAM industry in 2026. In terms of GB capacity, the demand for DDR storage corresponding to AI servers is expected to increase by 105% year-on-year in 2026, while HBM demand is projected to grow by 110% year-on-year. Both categories of memory products are maintaining a high-speed, doubling growth trend.

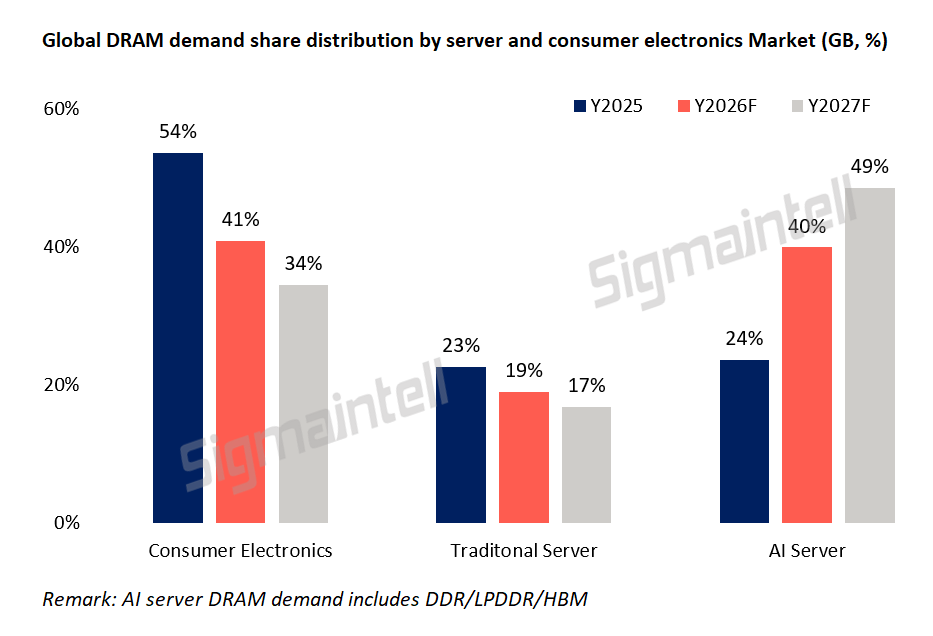

From the perspective of demand share, the proportion of total global DRAM output capacity (in GB) attributed to AI servers will exceed 40% in 2026, significantly surpassing the demand share of single categories like consumer electronics or traditional servers. Furthermore, the growth trend of AI servers is sustainable. It is anticipated that by 2027, the share of DRAM capacity demand from AI servers will climb to 49%, approaching half of the industry's total demand, indicating a strong upward trend in storage demand from the computational power side.

In the long term, the high demand for AI computational power will persist, with no significant decline expected in the industry demand between 2027 and 2028. It is projected that by 2028, the demand share of AI servers in the DRAM market will exceed 50%, settling within a range of 50% to 55%, thereby officially dominating DRAM industry demand.

Under the continued expansion and squeezing effect of AI server demand, the share of consumer electronics in the DRAM product structure will continue to decline. The most notable change will be seen in the DRAM demand share of smartphones, which is expected to drop sharply from 43% in 2024 to 23% in 2027. The consumer electronics industry faces significant supply constraints, directly prompting a reallocation of DRAM production capacity further towards the AI computational power sector.

Regarding market concerns about the inflection point of AI server growth, based on Sigmaintell's forecast data, AI servers are still expected to maintain a double-digit growth rate from 2027 to 2028. Global AI server shipments are projected to approach 5 million units in 2028. The overall storage capacity follows a dual growth logic: on one hand, the total shipment volume of AI servers continues to expand; on the other hand, as the volume of Tokens processed by AI models increases substantially and the computational load on servers rises, the average storage capacity of DDR and HBM per unit increases year by year. These two factors jointly drive the continuous rise in capacity demand within the DRAM industry.

Sigmaintell believes that the core driver of AI server demand has shifted from "model training" to "widespread inference adoption + application penetration." GPU technology is supporting this transformation through architectural innovation, HBM iteration, and computational breakthroughs. Over the next 3-5 years, the growth rate of computational demand may slow, but the absolute volume will continue to increase until new computational paradigms (such as quantum computing) mature.