Tag :Display

Time :2026-6-15

Core Insights:

> Multiple Factors Weigh Down Utilization Rate of Domestic FOLED Fabs.

> Global smartphone panel shipments stayed stable in Q1 2026. The transformation of set strategies has unleashed new growth momentum for FOLED panels.

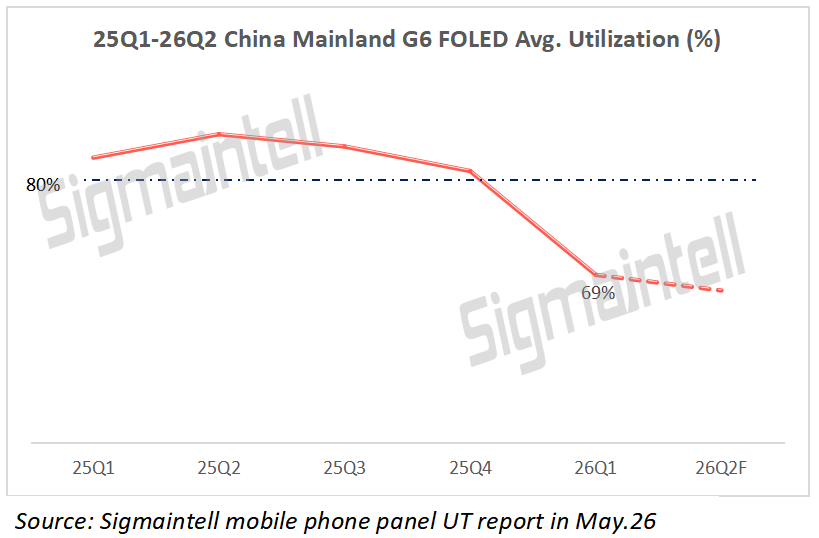

Multiple Factors Weigh Down Utilization Rate of Domestic FOLED Fabs.

In Q1 2026, the utilization rate of domestic G6 FOLED production lines in mainland China was under pressure due to multiple factors. First, inventories built up at the end of 2025 have not been fully digested, and terminal brands slowed down panel procurement significantly in the first quarter. Second, overall global demand for smartphones declined, leading to continuous order contraction.

Affected by the above dual pressures, the average utilization rate of domestic G6 FOLED production lines stood at 69% in Q1 2026, a notable drop from 80% in Q4 2025. Utilization rates of nearly all domestic panel production lines declined to varying degrees, and the whole industry operated at a medium-to-low level with a general downward trend.

Sigmaintell forecasts that in Q2 2026, although restocking demand for entry-level and mid-range models from individual brands will offer temporary support to the industry utilization rate, overall demand for finished handsets will remain sluggish. The average utilization rate of domestic G6 FOLED production lines will edge down by 2 percentage points QoQ to 67%, staying largely flat with the first quarter.

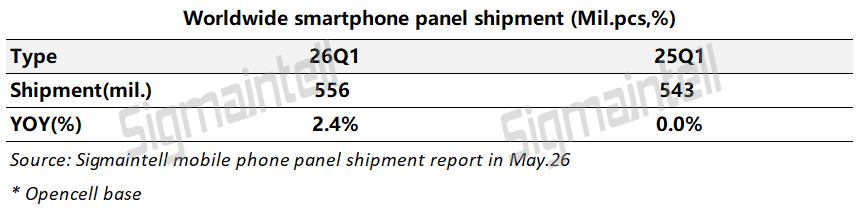

Global smartphone panel shipments stayed stable in Q1 2026. The transformation of set strategies has unleashed new growth momentum for FOLED panels.

According to Sigmaintell, global smartphone panel shipments reached 560 Mil.pcs in Q1 2026, representing a YoY increase of 2.4%. The growth was mainly driven by two factors: First, rising handset sales of Apple and Samsung boosted shipments of FOLED panels. Second, driven by higher memory chip prices, mobile phone retail prices went up generally, postponing device replacement demand. Meanwhile, panel procurement demand from the mobile phone repair market grew notably.

Against the backdrop of weakening overall demand for smartphone devices, LCD panels offset market pressure via applications in automotive, IT and other mid-size display sectors. However, the average utilization rate of FOLED production lines is unlikely to rebound to a high level in the short term, and competition among domestic panel manufacturers has intensified.

In addition, memory chip prices rose sharply beyond expectations, narrowing the pricing gap between different display technologies and weakening the cost advantages for set brands. The industry competition has shifted from cost-oriented to value-driven. To cope with rising upstream costs, terminal brands tend to enhance product competitiveness to boost handset sales and raise product prices.

Facing prolonged industry headwinds, set brands have adjusted their screen product layouts. Competition is no longer merely focused on panel cost bargaining, but places more emphasis on display performance, user experience and differentiated capabilities. High refresh rate, high brightness and low-power consumption high-end FOLED panels have become core competitive advantages for products. The downward penetration of such advanced technologies is expected to become a key driver for the recovery of utilization rates of FOLED production lines.